Health-Care Real Estate Deals Hit Record $26 Billion

Health-care real estate continues to thrive, and investors can’t get enough of the sector, according to JLL’s Valuation Advisory Group’s inaugural Healthcare Investor Survey and Trends Outlook.

Transactions in the sector climbed to $26 billion in 2022, marking an annual record.

In the first report of its kind for JLL, the commercial real estate services firm queried approximately 130 influential leaders in the health-care industry. Participants included private capital providers, which accounted for the highest representation at 33 percent, followed by developers and institutional investment managers, which comprised a respective 23 percent and 19 percent of respondents. The group helped provide a crystal-clear picture of health-care real estate’s success in 2022 and its prospects in 2023.

According to the JLL report, medical office buildings proved a powerful magnet for investors in 2022, with the property type accounting for 58 percent of overall health-care investment activity. Part of the high volume of trading in the sub-sector can be attributed to the $9.4 billion merger between Healthcare Realty Trust and Healthcare Trust of America, which involved a portfolio of approximately 400 MOBs. Had the joining of the two companies not occurred, the numbers would likely look a bit different, as transaction activity declined significantly in the fourth quarter of 2022 due to pricing uncertainty amid rising interest rates and recession fears.

Ambulatory surgical centers followed MOBs in popularity among investors in 2022. Trades involving the property type went on the upswing, jumping 7 percent year-over-year to 27 percent of the total health-care transactions. The investment community’s keen interest in MOBs and ASCs can be linked to an ongoing transformation that has buoyed demand in the outpatient care arena.

“Advances in technology, changes in reimbursement and consumer preference and convenience have shifted sites of care from inpatient to outpatient,” according to the JLL report.

Fundamentally Sound

The rising demand for MOBs along with a low level of new deliveries are serving as a foundation for strong fundamentals in the sector. At the close of 2022, MOBs recorded an occupancy level of 92.3 percent and continued to experience consistent rent growth. MOBs are outperforming the traditional office sector, where the average occupancy level is a notable 11.4 percent lower.

Unlike traditional office buildings, MOBs are not contending with the leasing challenges that accompany the spread of the remote-work trend. And the very nature of MOB space lends itself to longer tenant commitments.

“Because of the high cost to build out a medical office space and proximity to patients, medical office tenants tend to remain in the same space for longer, providing stable occupancy,” as noted in the JLL report.

No Hindrance To Sunny Forecast

Although MOBs are the star of health-care real estate in investors’ eyes, the sector is not impervious to challenges. JLL queried survey respondents regarding their apprehensions about potential obstacles in the health-care investment sector over the next 12 months, and 66 percent pointed to rising interest rates and capital markets as the leading concern. Development costs, garnering the concern of 13 percent of respondents, ranked as the second-most worrisome issue.

Although the investment community is operating with the knowledge that looming obstacles could impact their activity, 66 percent of survey respondents reported that MOBs will remain the most desirable opportunity in health-care real estate in 2023. The immense appeal of MOBs among investors is here to stay for the long term, even amid economic uncertainties.

As noted in the JLL report, “Strong net operating income growth at 2.7 percent in the fourth quarter of 2022, despite high expenses and acceptance of 3 percent escalations, make MOBs a resilient asset class in a cloudy economic climate.”

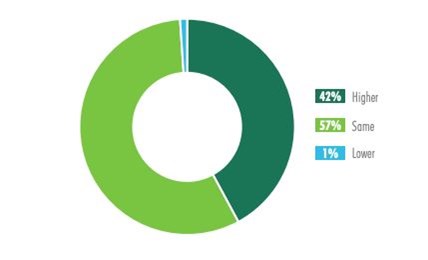

The future looks bright for health-care real estate investment overall. Thirty percent of survey participants indicated that they anticipate an increase in transaction activity and market valuations over the next 12 months.

Source: CPE