Healthcare REITs: Back On Life Support

The United States healthcare system has taken center-stage amid the coronavirus outbreak as Healthcare REITs have been on a roller-coaster ride amid evolving forecasts of the severity of the pandemic.

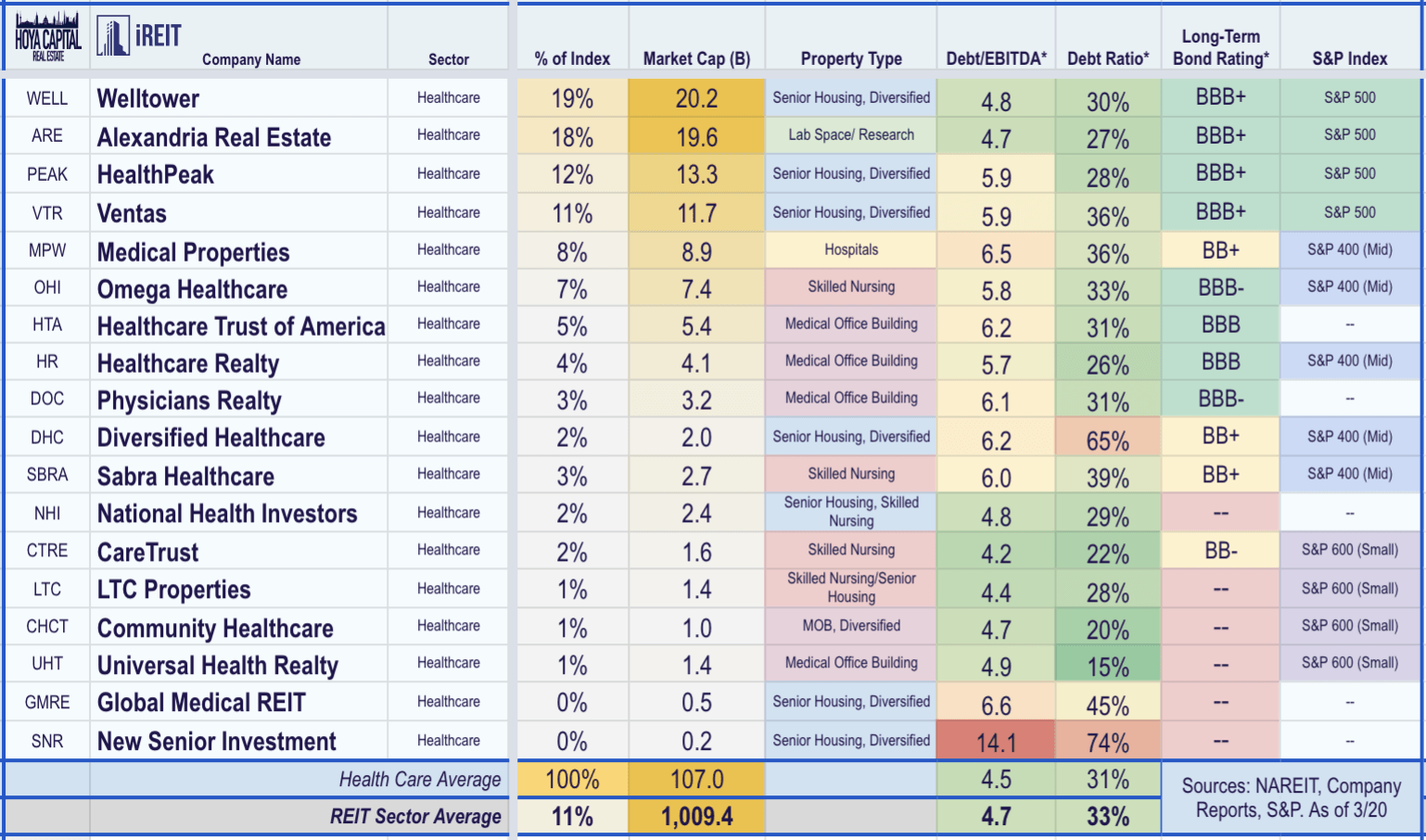

Within the Hoya Capital Healthcare REIT Index, all 18 healthcare REITs are tracked, which account for roughly $110 billion in market value. One of the higher-yielding and more defensive REIT sectors, Healthcare REITs comprise 10-12% of the broad-based “Core” REIT ETFs and are generally well-positioned to capture the demographic-driven tailwinds of the aging population over the next decade.

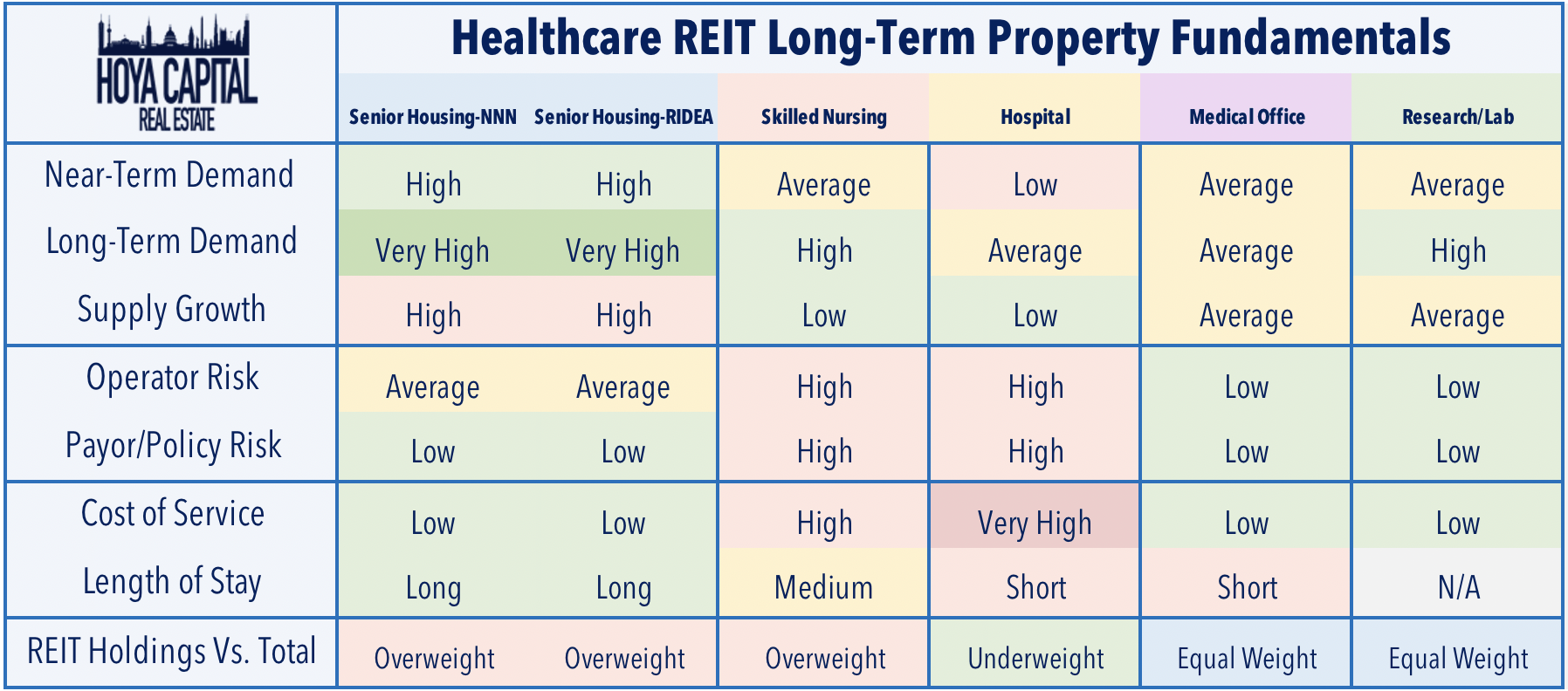

There are five sub-sectors within the healthcare REIT category, each of which have distinct risk/return characteristics. The senior housing sector can be further split into two categories based on lease structure: triple-net leased properties or SHOP (senior housing operating properties). For senior housing, supply growth has been a lingering headwind that has pressured occupancy and rent growth in recent years. Policy-risk is an important factor for skilled nursing and hospital REITs, which derive a significant portion of their revenue from public and private health insurance reimbursements. These “public pay” REITs have been pressured in recent years by policy changes that have attempted to push patients into lower-cost healthcare settings. Medical office and research/lab space, meanwhile, have generally exhibited the most steady and consistent fundamentals within the healthcare REIT space.

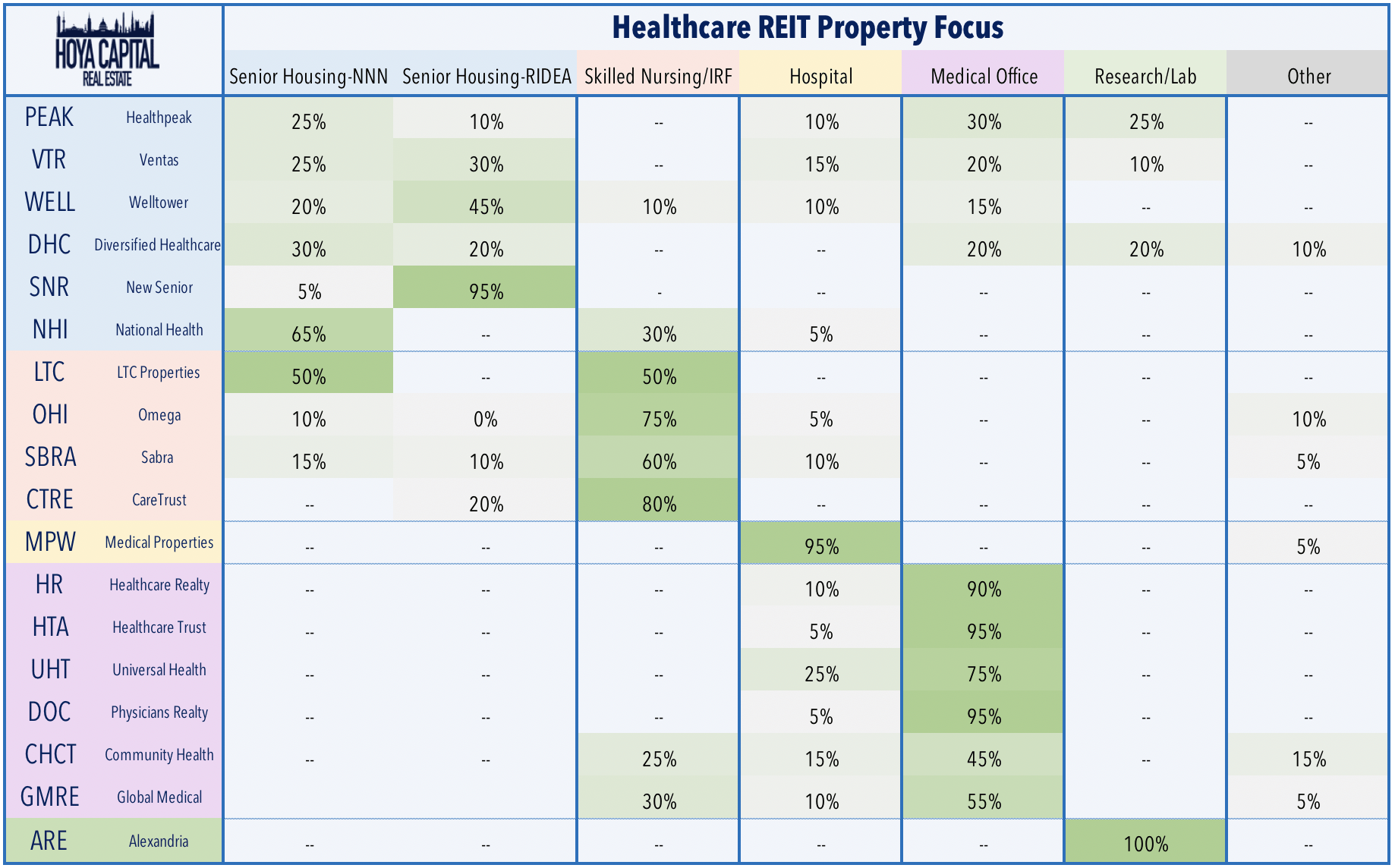

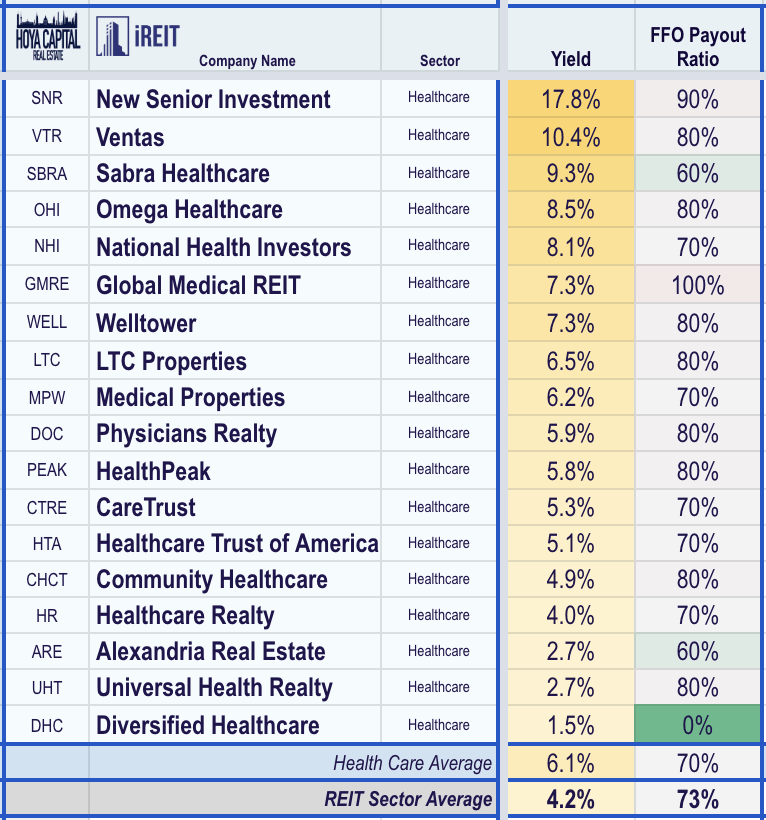

Healthcare REITs tend to focus on a single property type and are led by the “Big Three” healthcare REITs – Ventas (VTR), Welltower (WELL), and Healthpeak (PEAK). These “Big 3” REITs hold a fairly diversified portfolio across the healthcare spectrum, although these firms have divested most of their public-pay assets in recent years to focus more exclusively on the senior housing sub-sector. Other players in the senior housing space include New Senior (SNR), National Health (NHI) and Diversified Healthcare (DHC). On the public-pay side, the skilled nursing sub-sector includes Omega Healthcare (OHI), Sabra Health Care (SBRA), CareTrust (CTRE), and LTC Properties (LTC) while there is a single hospital-focused REIT, Medical Properties (MPW). The medical office sub-sector includes Healthcare Realty (HR), Healthcare Trust (HTA), Universal Health (UHT), Physicians Realty (DOC), Community Healthcare (CHCT), and Global Medical REIT (GMRE). Alexandria Realty (ARE), meanwhile, is the lone REIT focused exclusively on research and lab space.

Still a relatively fragmented industry, Healthcare REITs own approximately one-tenth of the total $2 trillion worth of healthcare-related real estate assets in the United States. Occupancy in senior living facilities is generally “by necessity” and the average age of occupants in these facilities is roughly 84 years old. Healthcare REITs have historically been among the most active acquirers and consolidators, using the competitive advantages of their REIT structure to fuel accretive external growth. Healthcare REITs primarily lease properties to tenants under a long-term triple-net lease structure, though these REITs have taken on increasingly more operating responsibilities over the past decade as these they attempt to mitigate the risks of their third-party operators, many of which have struggled to remain profitable in recent years amid rising costs and lower reimbursement rates. Healthcare REITs have historically been a defensively-oriented sector that pays hearty dividend yield.

Healthcare REITs Slammed By Coronavirus Pandemic

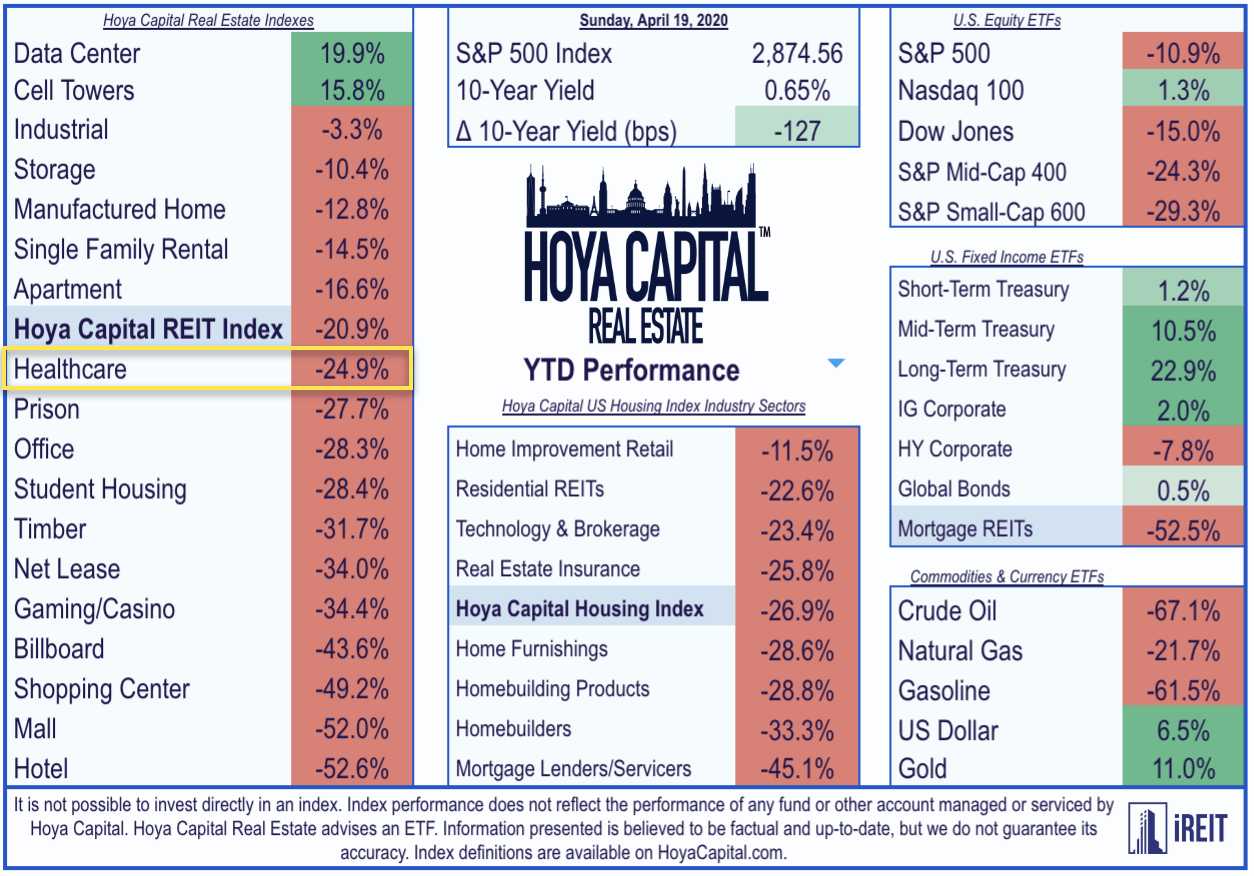

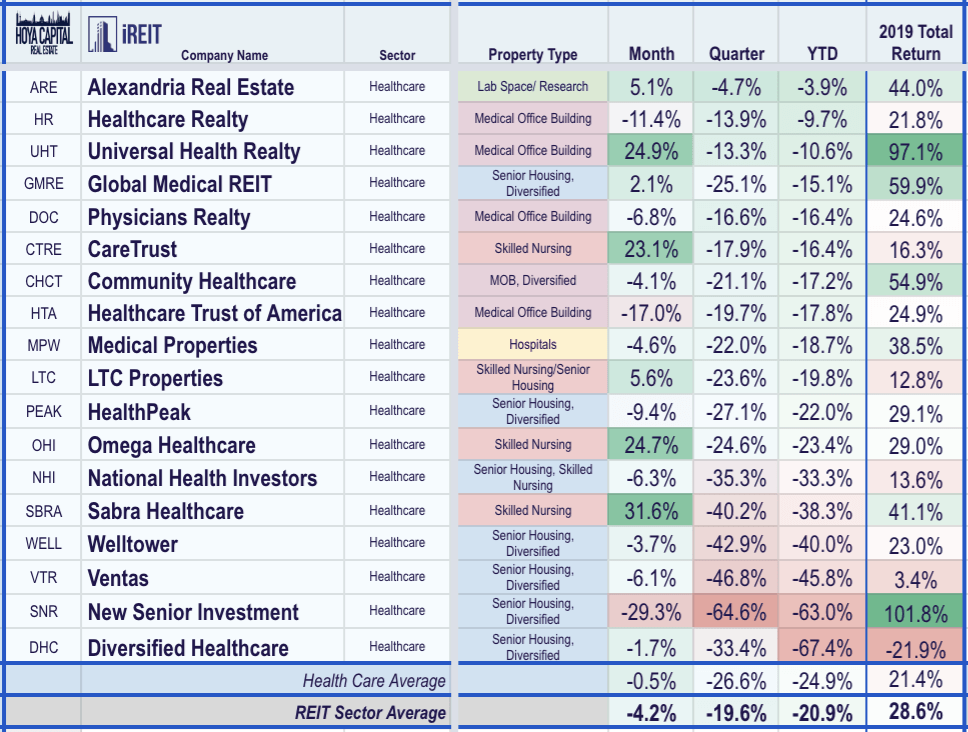

Healthcare REITs were slammed during the early-onset of the outbreak but have recovered in recent weeks as death rate estimates have, thankfully, been revised drastically lower from early catastrophic figures. At their lows on March 23, the healthcare REIT sector was off by roughly 45% on the year with several small-cap names down more than 75%, but these REITs have clawed back nearly half of these losses over the last three weeks as coronavirus forecasting models evolved and updated. For the year, the Hoya Capital Healthcare REIT index is lower by 24.9% compared to the 20.9% decline on the broad-based REIT average and the 10.9% decline on the S&P 500.

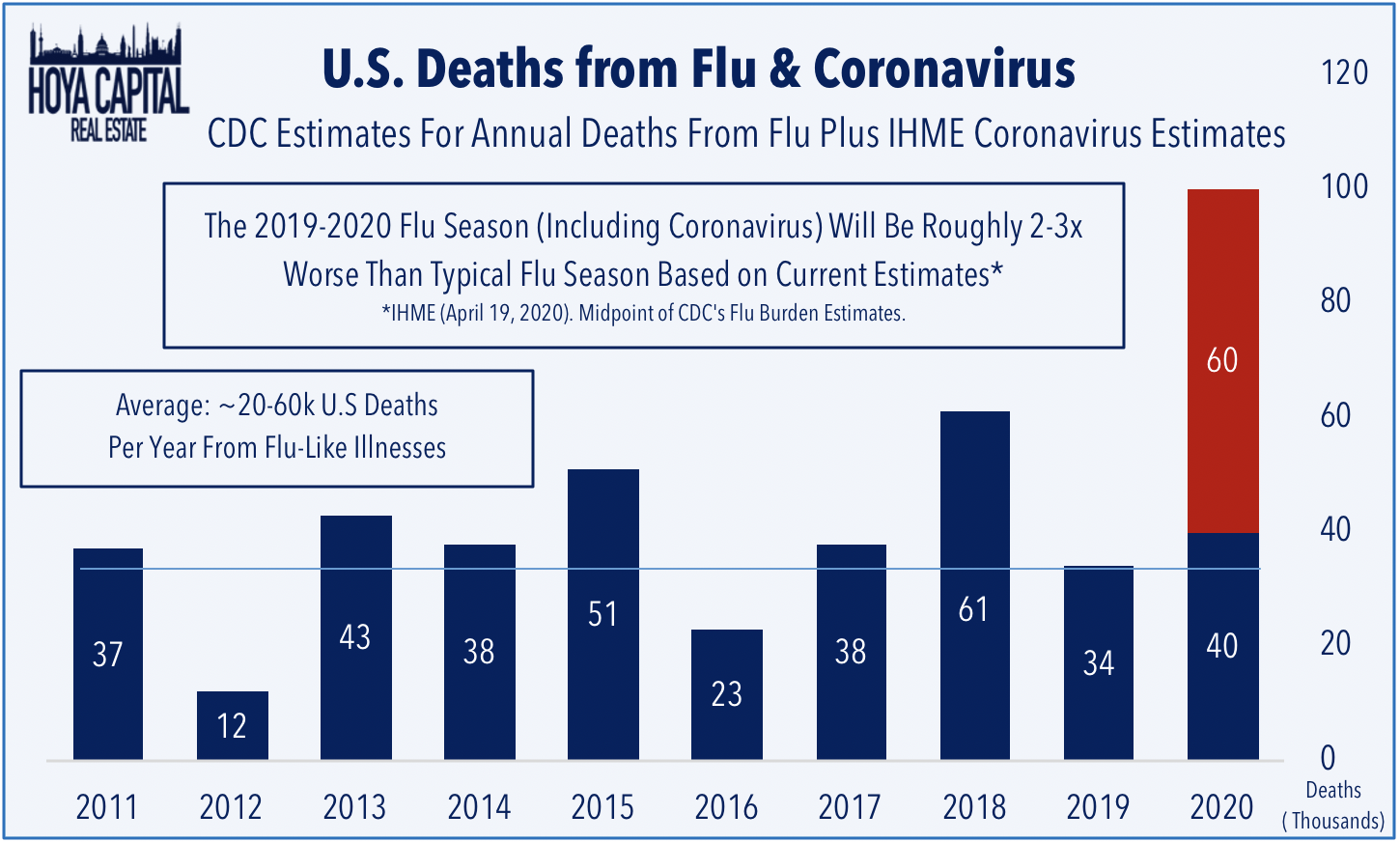

The Institute for Health Metrics and Evaluation (IHME) now estimates that there will be 60,308 COVID-19 deaths, significantly lower than the 240,000 estimate just a month ago. Concerns about the severity of any given flu season is an annual issue for healthcare real estate investors – particularly senior housing and skilled nursing operators – who unfortunately see thousands of resident deaths per year. A typical flu season in the United States will result in between 20,000-60,000 deaths every year according to the CDC, with 95% of deaths above the age of 65. Using current estimates from the CDC and IHME, the 2020 flu season – including the impacts of coronavirus – will likely be 2-3x worse than the typical year and skewed more heavily towards older age cohorts which have been hit disproportionately hard.

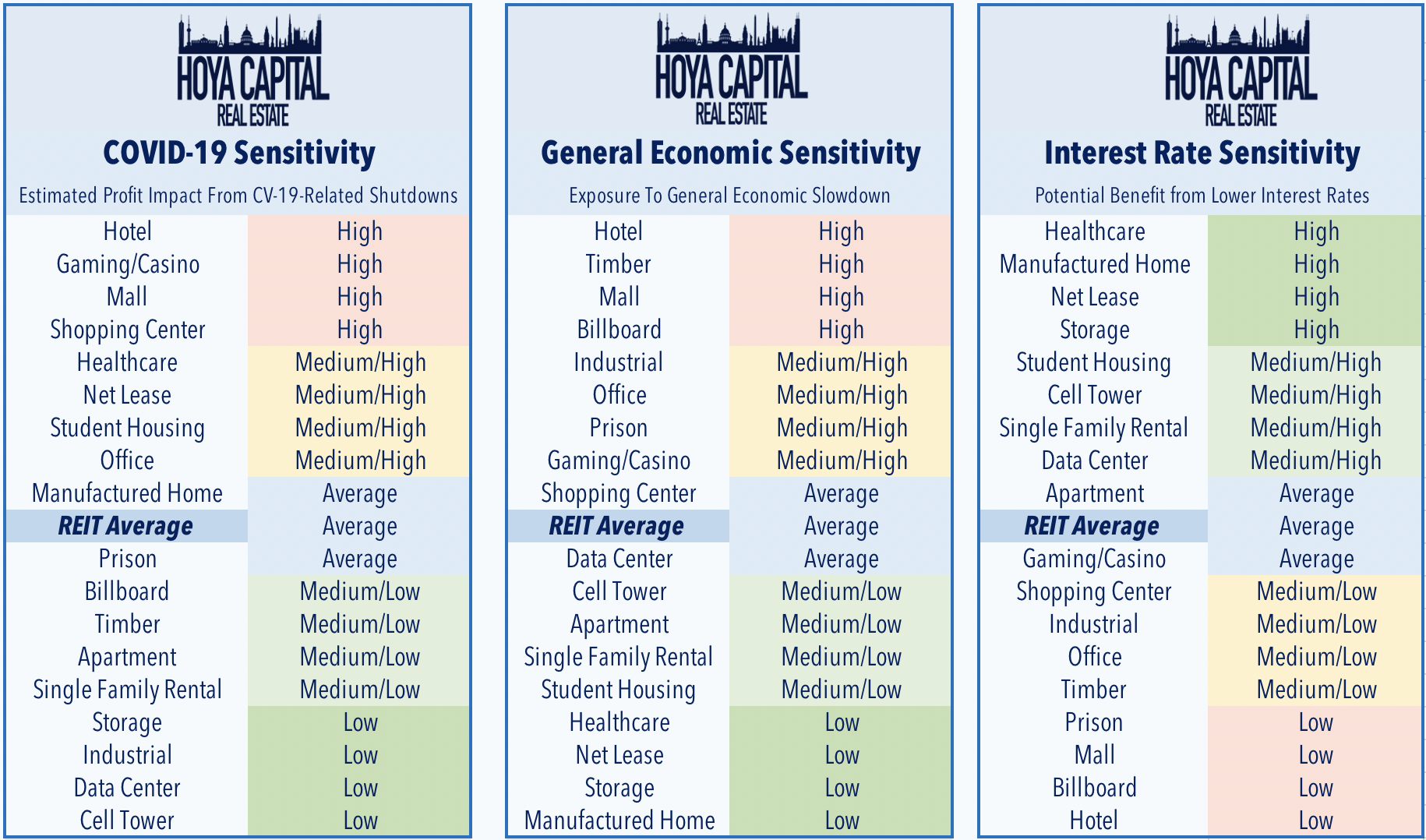

While likely less devastating on underlying demographics than once feared, no healthcare real estate sector – or any REIT sector for that matter – is immune from the significant near-term and long-term effects of the pandemic. Below is a framework for analyzing the REIT property sectors based on their direct exposure to the anticipated COVID-19 effects as well as their general sensitivity to a potential recession and impact from lower interest rates. Within the COVID-19 sensitivity chart, healthcare REITs are the fifth-most exposed sector to according to our estimates behind hotel, gaming, and retail REITs. Healthcare REITs, however, are usually one of the more stable sectors during “garden variety” economic downturns due to their long-lease terms and generally stable demand profile.

While likely less devastating on underlying demographics than once feared, no healthcare real estate sector – or any REIT sector for that matter – is immune from the significant near-term and long-term effects of the pandemic. Below is a framework for analyzing the REIT property sectors based on their direct exposure to the anticipated COVID-19 effects as well as their general sensitivity to a potential recession and impact from lower interest rates. Within the COVID-19 sensitivity chart, healthcare REITs are the fifth-most exposed sector to according to our estimates behind hotel, gaming, and retail REITs. Healthcare REITs, however, are usually one of the more stable sectors during “garden variety” economic downturns due to their long-lease terms and generally stable demand profile.

The effects of the pandemic will be felt in different intensities within each healthcare real estate sub-sector. Amid the ongoing lockdowns, senior housing REITs have seen occupancy decline due primarily to depressed move-in rates and a sizable uptick in expenses in efforts to prevent and/or control the spread of the virus within the community. Long-term attitudes and behaviors towards senior housing – particularly in independent living communities – may be affected as well. For skilled nursing REITs, the pandemic further exasperates issues with their troubled operators, who have seen expenses rise significantly, a near-term issue that could very well become a long-term risk. For hospitals, the suspension of elective surgeries and a far lower-than-expected surge of coronavirus patients has stretched the already-tight budgets of hospitals and led to tens of thousands of layoffs of doctors and nurses. For the medical office category, while near-term risks are minimal, the huge uptake in usage of telemedicine may alter the long-term need for MOB space.

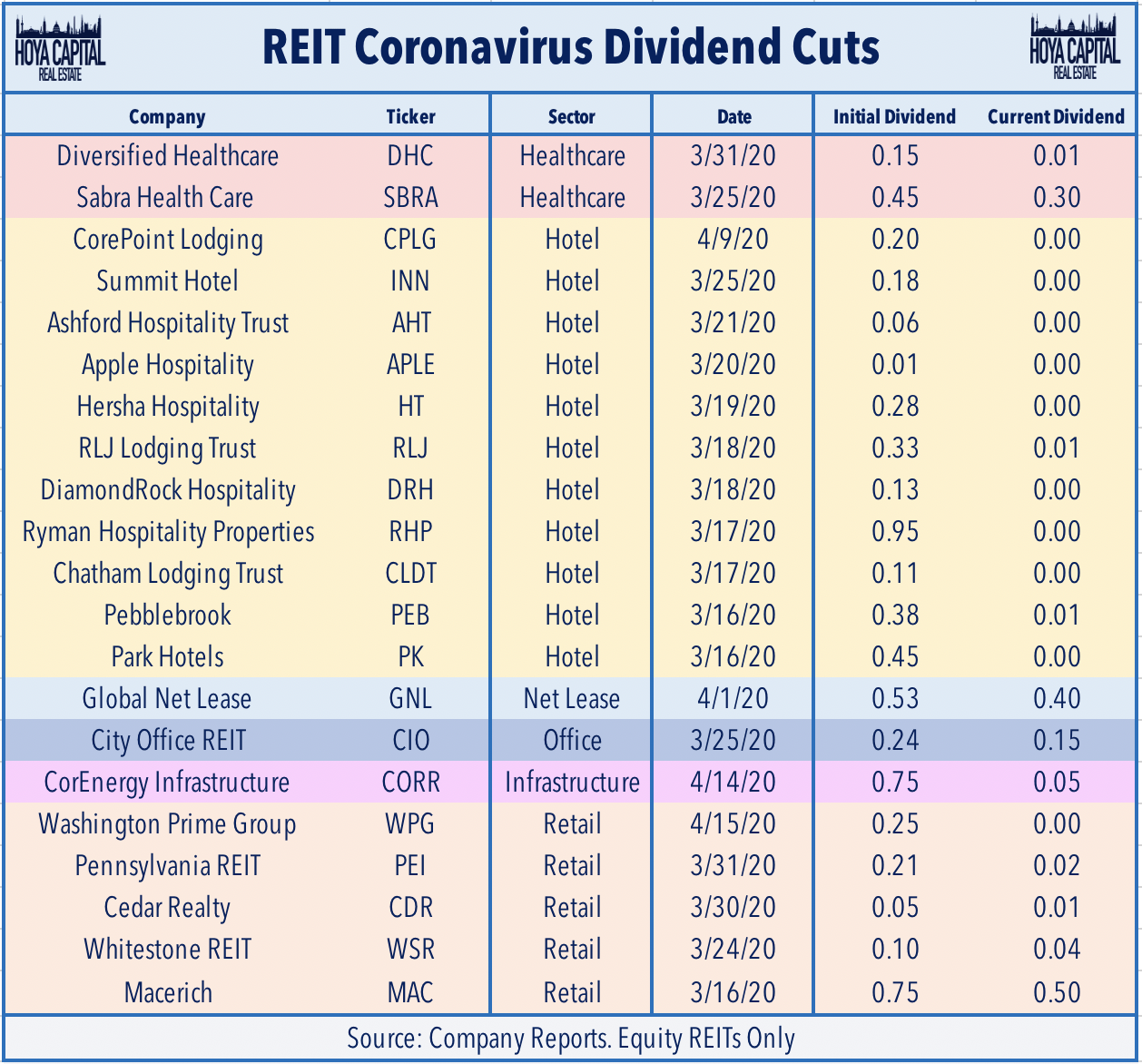

Naturally, the relatively more immune research/lab space and medical office-focused REITs have outperformed amid the pandemic with Alexandria Realty, Healthcare Realty, and Universal Health Realty leading the way this year. Senior housing-focused REITs, particularly small-cap New Senior and Diversified Healthcare, have been hit especially hard since the start of the outbreak and have yet to enjoy a similar bounce-back as the rest of the sector. So far, two healthcare REITs – Sabra Healthcare and Diversified Healthcare – have announced dividend cuts anda few more expected once earnings season kicks-off next week in what will surely be an eventful and newsworthy few weeks. We’ll have full real-time coverage of earnings season on iREIT on Alpha and as well as in our Real Estate Weekly Outlook.

Long-Term Outlook Remains Mostly Intact

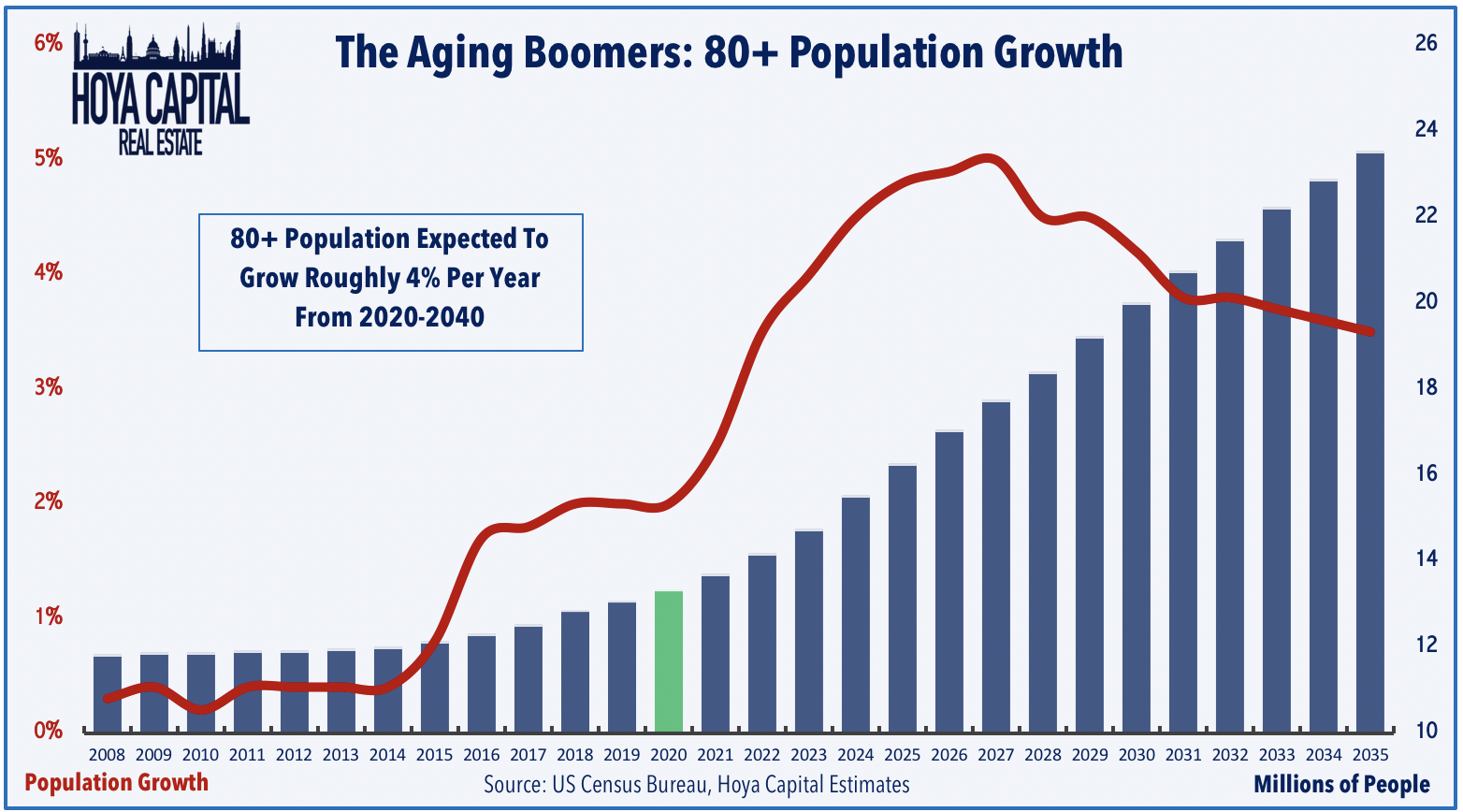

For healthcare REITs, the long-awaited demographic-driven demand boom from the aging Baby Boomers – a historically large generation generally defined as those born between 1945 and 1965 – is finally on the horizon. While there was significant fear last month that the contours of this generation could be materially altered by the coronavirus pandemic, current forecasts thankfully suggest a more muted impact. Following the relatively small “Silent Generation,” Baby Boomers are a healthier and wealthier cohort, expected to live longer lives and consume healthcare at a rate that significantly exceeds their prior generational peers. After years of relative stagnation in the critical 80+ population cohort for healthcare real estate, the long-awaited demographic boom is finally in sight as this age segment will nearly double over the next 30 years and grow at an estimated 4% per year through 2040.

Early hints of this long-awaited demand boom were just showing hints of emerging at the end of 2019. According to recently-released NIC data, 2019 was the first year since 2015 to have seen a sequential uptick in average occupancy for senior housing and the first year since 2005 to see an uptick for skilled nursing. While wage pressures continue to pressure margins and rent growth remains uninspiring at inflation-matching levels, same-store NOI performance in 2019 appeared to be an inflection point for the long-sagging healthcare sector. In 4Q19, same-store NOI growth rose to the strongest TTM growth rate in nearly three years at 1.48% following three years of deteriorating performance. Several unknown variables will determine the extent of the coronavirus-related slowdown in 2020, primarily related to the length and severity of the pandemic and if it results in any “permanent” damage to key tenants that would require restructuring.

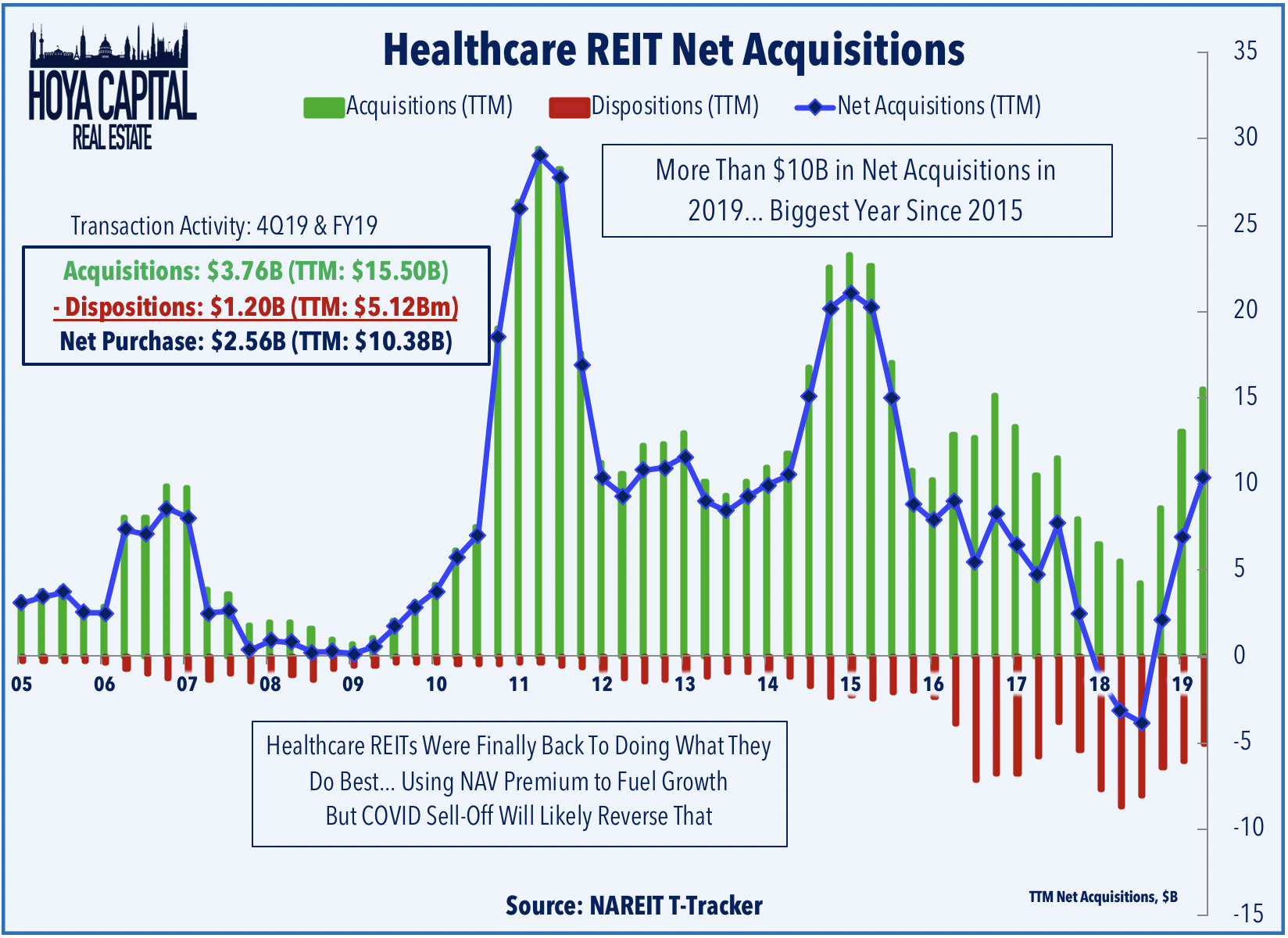

Normally, a “garden-variety” recession would be associated with relative outperformance from the healthcare REIT sector. After the prior recession, healthcare REITs went on a buying spree, acquiring tens of billions of dollars worth of healthcare assets from weaker and more troubled operators. This accretive external growth was harder to come by over the last half-decade, but strong share price performance over the last two years had restored the sector’s coveted NAV premium, allowing these REITs to get back to doing what they do best. Healthcare REITs acquired more than $10 billion in net assets in 2019, which was the largest since 2019. The coronavirus pandemic, however, has quickly flipped these sizable NAV premiums to similarly-sized NAV discounts, which will likely reverse the recent momentum.

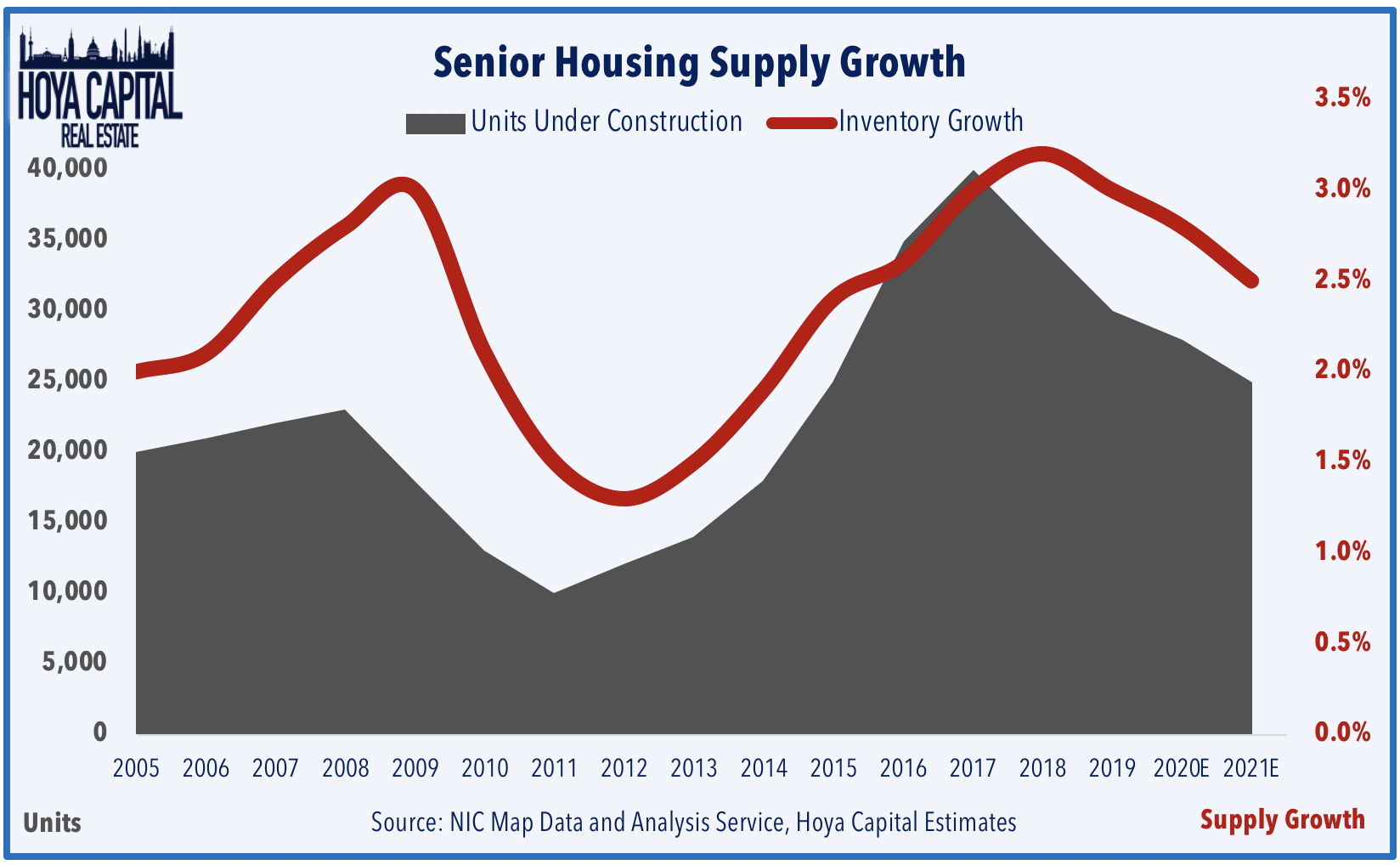

The ‘Aging Boomer’ investment thesis has been no secret to developers as senior housing has been one of the few housing segments seeing ample speculative supply growth in preparation for aging boomers, defying the broader “housing shortage” theme of limited supply in the entry-level and mass-market housing segments. While demand has been predictably steady and showing early signs of Boomer-led acceleration for most sub-sectors outside of skilled nursing, relentless supply growth over the past several years has continued to pressure same-store NOI growth for the senior housing sector. Absent the coronavirus outbreak, it was projected that in 2020 would see roughly supply/demand equilibrium followed by a decade of demand growth outpacing supply growth. That supply/demand equilibrium will likely be pushed back to 2021 given the likely near-term contraction in demand amid the ongoing lockdowns.

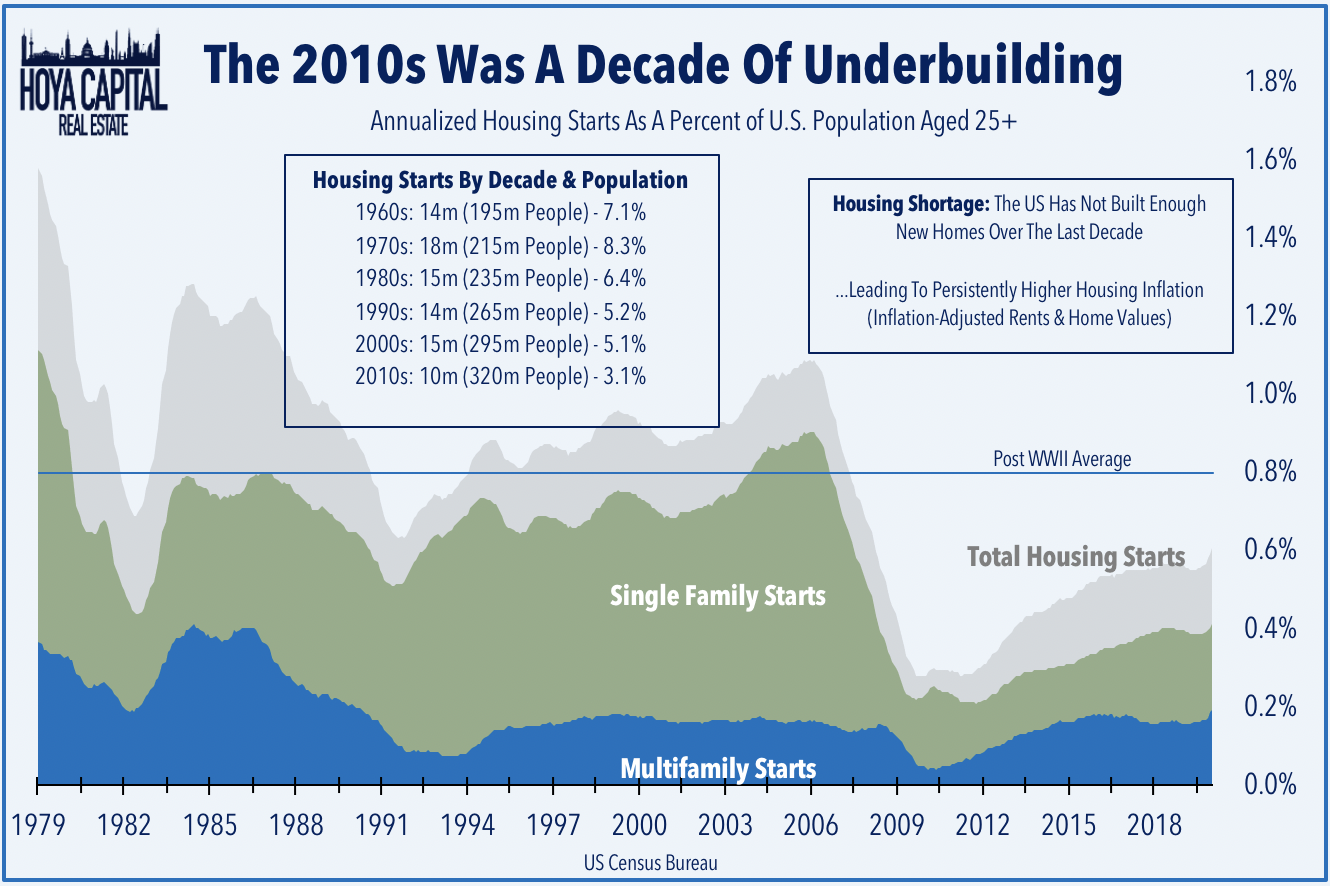

The relative oversupply of purpose-built senior housing, however, needs to be viewed in the context of the broader housing market. CBRE estimates that there are roughly 3 million professionally-managed senior housing or skilled nursing units in the US, representing less than 2% of the total US housing stock. By nearly every metric, the U.S. housing markets remain significantly undersupplied at the national-level after a decade of historically low levels of residential fixed investment. As discussed in the focus of our last healthcare REIT report, this has important implications for the retirement prospects of millions of aging Boomers. It is believed that the fears of a “retirement crisis” are overstated due in large part to rising home values over the past decade as Americans – mostly Boomers – who have built up $10 trillion in additional home equity over the last decade which can be tapped over the next decade to pay for healthcare services.

Healthcare REIT Valuations & Dividends

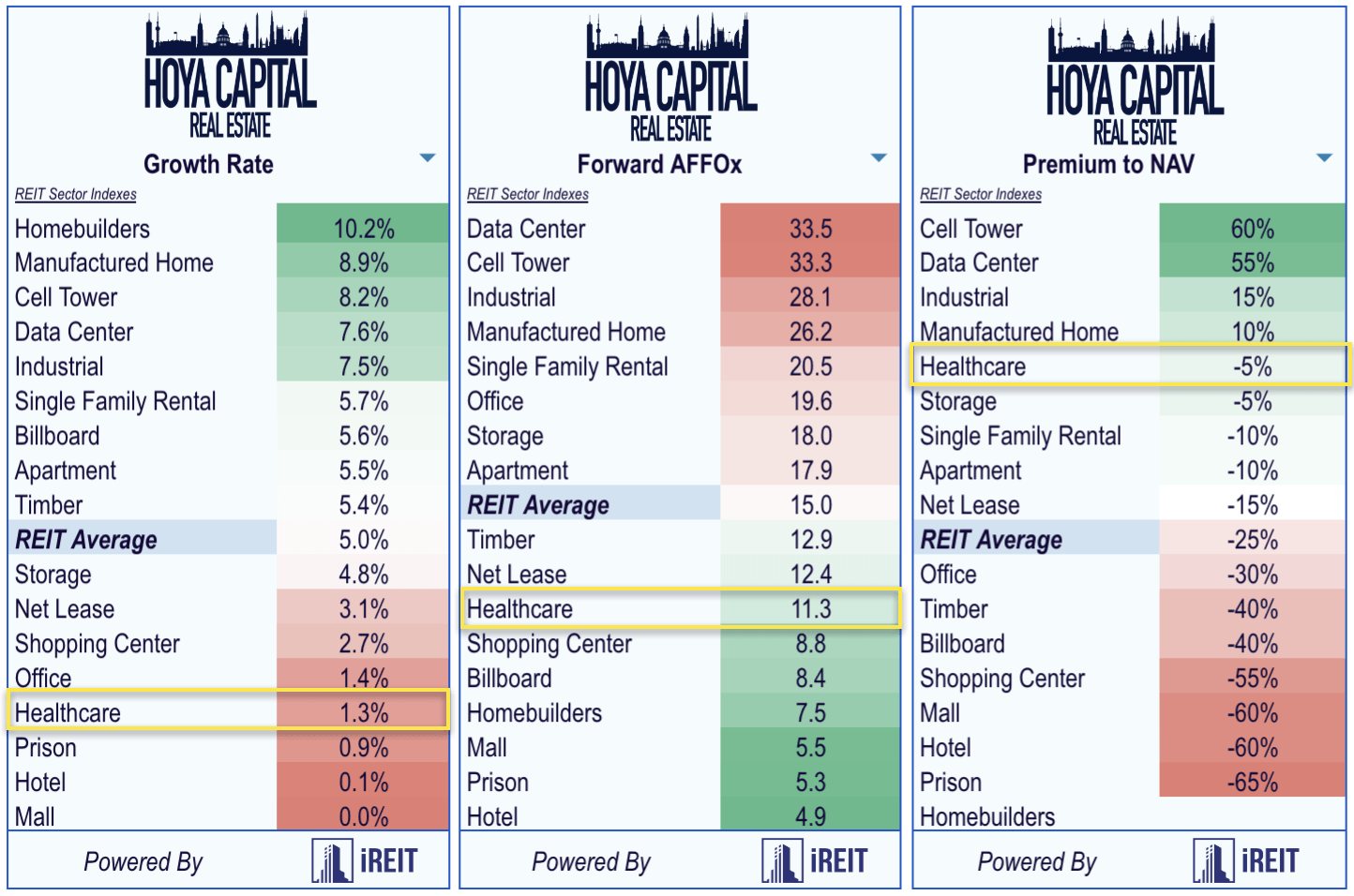

Healthcare REITs currently trade near the lowest valuations seen over the last decade, and continue to trade at discounted valuations relative to other REIT sectors based on consensus Free Cash Flow (aka AFFO, FAD, CAD) metrics. Trading at roughly an 11x AFFO multiple, healthcare REITs trade well below the 15x REIT sector average. Powered by the iREIT Terminal, the sector now trades at a roughly 5-10% discount to Net Asset Value, a reversal from the NAV premium seen at the end of 2019.

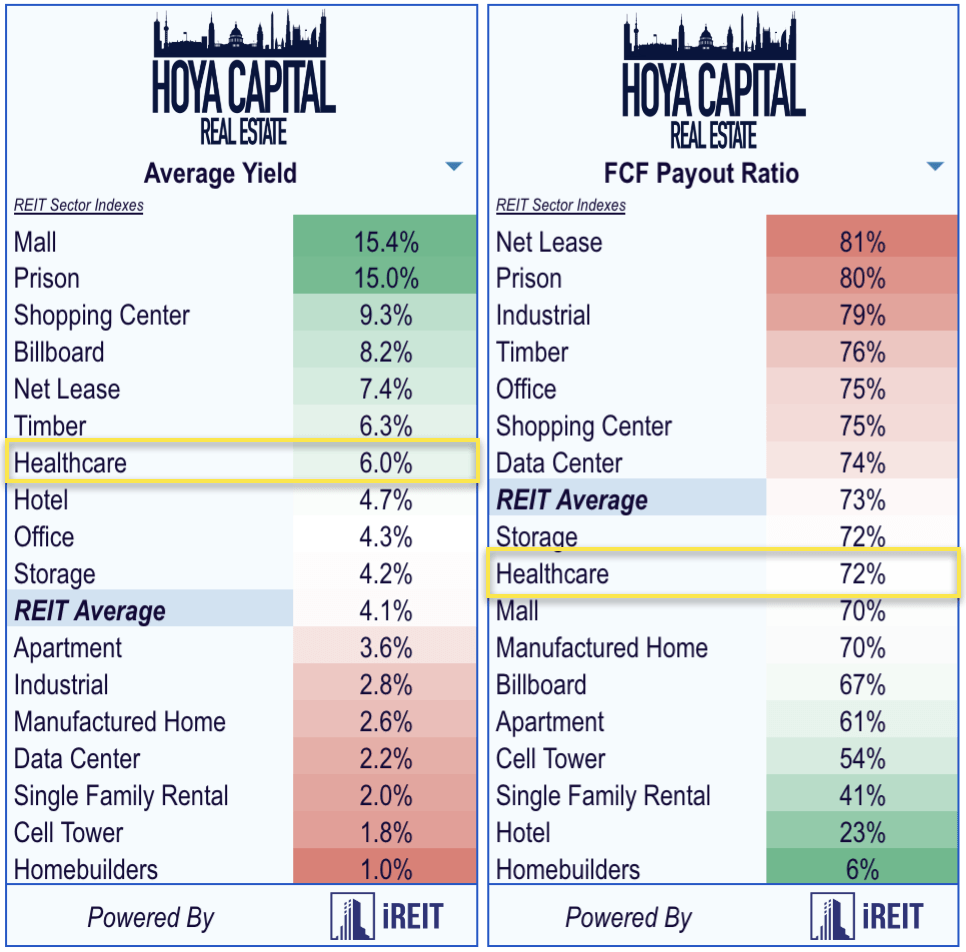

Healthcare REITs have historically been strong dividend payers and continue to rank towards the top of the REIT sector in that regard even after two of the eighteen REITs cut their dividends last month. Healthcare REITs pay an average yield of 6.0%, which is above the REIT sector average of 4.1%. Healthcare REITs, on average, payout roughly 75% of their available cash flow, which leaves some cushion to maintain dividends, though several REITs are at higher risk of dividend cuts due to their already extended payout ratios.

Dividend yields of the individual names in the healthcare REIT sector range from a low of 1.5% (Diversified Healthcare, which cut its dividend last month to preserve cash) to a high of 17.8% (New Senior Investment). SNR and GMRE as the two most at-risk for a dividend cut based on extended payout ratios, which may be announced during earnings season over the next few weeks. Investors seeking a safe, predictable income stream should focus on the MOB, lab/research, and upper-tier senior housing healthcare REITs such as the Big 3 (Welltower, Ventas, and HCP), Healthcare Trust, Healthcare Realty, Physicians Realty, or Alexandria. Investors who are looking willing to take on significant speculative policy and operational risk can take a look at the primarily public-pay REITs such as Omega, Medical Properties, and Sabra.

In a recent report, “The REIT Paradox: Cheap REITs Stay Cheap“, the study that showed that lower-yielding REITs in faster-growing property sectors with lower leverage profiles have historically produced better total returns, on average, than their higher-yielding and higher-leveraged counterparts. We’ve now tracked 22 equity REITs in our universe of 165 names to announce a cut or suspension of their dividends in addition to the roughly half of mortgage REITs (20 out of 41) that have announced dividend cuts thus far. So far, all of the dividend cuts or suspensions have come from sectors that are deemed as High or Medium/High COVID-19 risk.

Key Takeaways: Back on Life Support, But Not Terminal

The United States healthcare system has taken center-stage amid the coronavirus outbreak. Healthcare REITs have been on a roller-coaster ride amid evolving forecasts of the severity of the pandemic. Healthcare REITs were slammed during the early-onset of the outbreak but have recovered in recent weeks as death rate estimates have, thankfully, been revised drastically lower from early catastrophic figures.

While likely less devastating on underlying demographics than once feared, no healthcare real estate sector is immune from the significant near-term and long-term effects of the pandemic. For senior housing, skilled nursing, and hospital REITs already dealing with soft underlying fundamentals, the pandemic will put a sizable dent in near-term demand and drive significantly higher expense growth. The positive long-term outlook for senior housing remains intact as the long-awaited demographic-driven demand boom is finally arriving. Behaviors and attitudes towards senior housing and telemedicine, however, shouldn’t be overlooked.

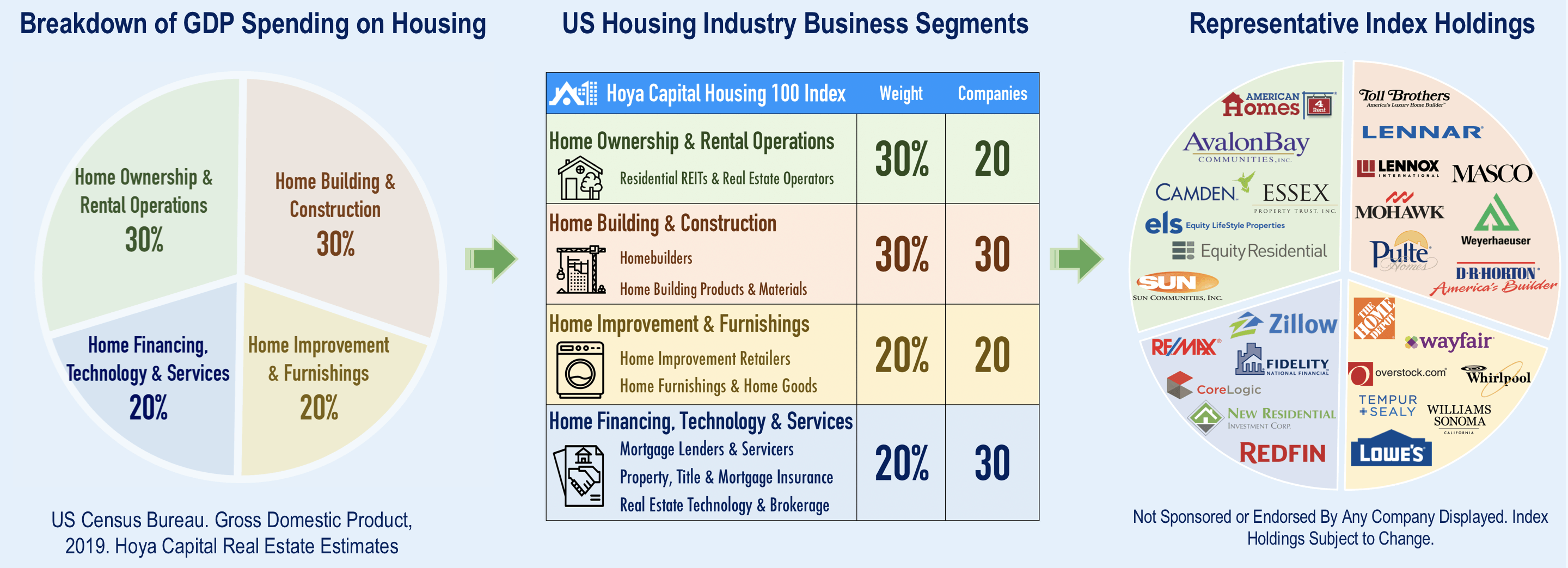

Investors seeking to play the sector through an ETF can take a look at the Long Term Care ETF (OLD), which allocates roughly 50% of its holdings towards senior housing and skilled nursing REITs or the iShares Residential REIT ETF (REZ), which allocates roughly 30% towards healthcare REITs, including medical office and hospitals. Senior housing REITs also compose roughly 4-5% of the Hoya Capital Housing Index, which tracks the performance of the U.S. housing industry. It is believed that the combination of historically low housing supply and strong demographic-driven demand provides a very compelling macroeconomic backdrop for the US housing industry – including senior housing – over the next decade.

I

I

Source: Seeking Alpha