Medical Real Estate Still The Best Way To Keep Your Portfolio Healthy

In 2018, the JSE’s SA listed property index dropped 25%. In 2019, the total return from the index was 1.92%, well below inflation. In the first five months of 2020, the index shed 39%.

Although dividends from listed property grew by 8-12% a year between 2014 and 2017, growth slowed to 3.5% in 2019, which again was below inflation. In response to the economic fall-out from Covid-19, many property companies have warned they will withhold dividends this year to strengthen their balance sheets and until they understand the full fallout from the pandemic.

The data is not looking encouraging. Office tenants are cutting space wherever possible, having learned that their reduced workforce can work from home. Retail is under enormous pressure across the board, from the legendary brands like Edgars to the smaller independent brands, and restaurants that just don’t have the fire power to recapitalise and pay rents in a market where there are still restrictions and the consumer is unable to come to the rescue.

What’s more, if you are in the hotel and hospitality industry, then there is really no clear path to recovery at this stage and the losses will be devastating.

There’s no refuge in residential property, either. The Lightstone Residential Property Index shows national house price growth in SA peaked at 6.25% in 2014 and has slowed since then to a five-year low of 1.7% in 2019. Lightstone expects, despite the recent interest rate cuts, that growth in the residential housing market will slow again in 2020.

Two specialized sectors of the property market have continued to deliver solid returns throughout the Covid-19 crisis. Logistics is one of the winners due to online e-commerce stores which have enjoyed a surge in online shopping.

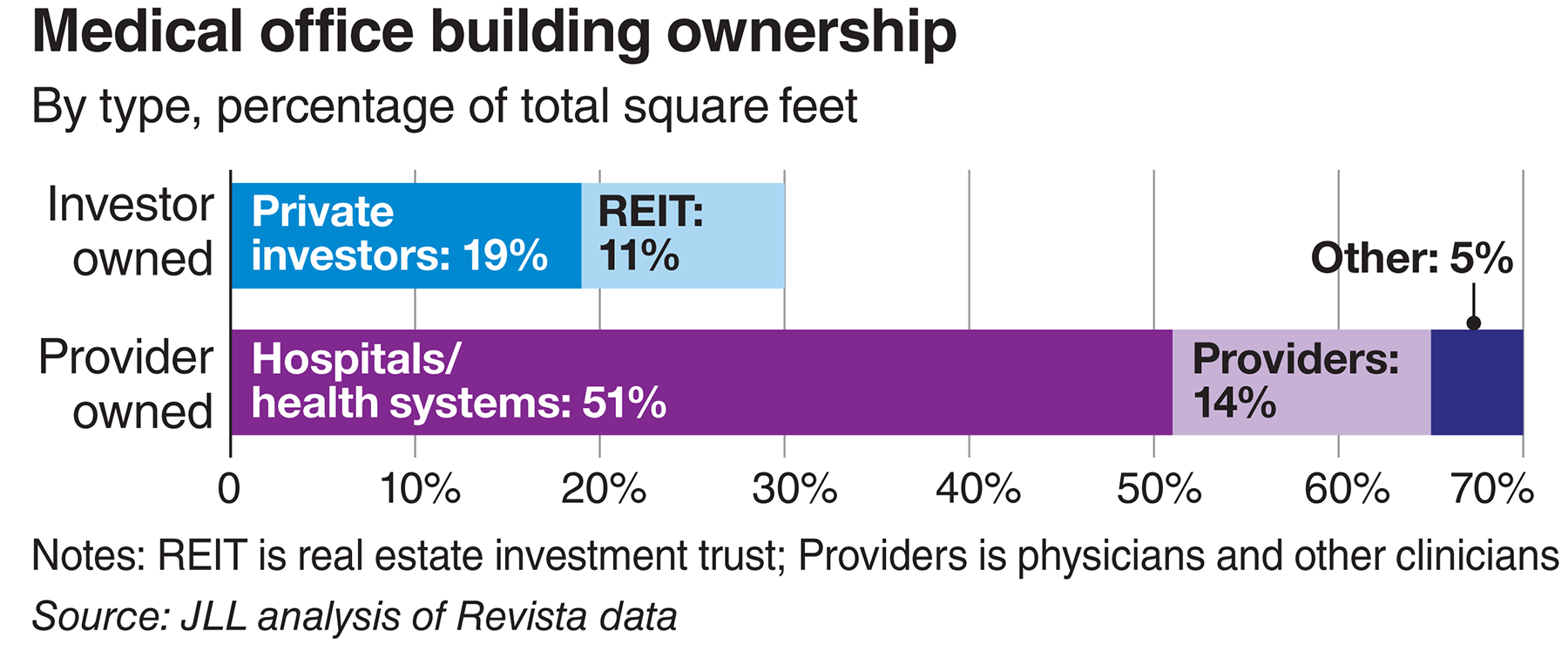

The other big winner globally is medical office buildings, whose tenants mostly offer essential services. Even those who had been required to close are already benefiting from a post-lockdown surge in patient visits as medical procedures can, in most cases, not be postponed indefinitely. Think for a moment about your dentist, who will still need to attend to those fillings even if he could not see you over the last three months.

For South Africans who invested in offshore logistics or medical buildings, the rand returns have been considerably enhanced by the latest depreciation of the rand against the dollar.

In the US, the Covid-19 crisis has hit particularly hard, with 134,000 deaths by early July, amid total confirmed cases exceeding three million. Hospitals under pressure to clear wards and scale up for the anticipated flood of Covid-19 patients have had to postpone all elective procedures and turn patients away who were not critical.

This dramatically affected the income of all medical professionals who are not directly involved in treating Covid-19 patients, and has also affected hospitals’ revenue. Even as the US emerges from lockdown, patients choose to avoid traditional hospitals in fear of being exposed to the virus. This has been a boost for medical practitioners working outside the hospital systems, as patients have sought treatment from doctors working from these independent facilities.

Orbvest, which has 19 medical office buildings under management in three US states (Texas, Georgia and New Jersey), noted rental collections declined slightly in April, during lockdown, as about 21 tenants across the entire portfolio of over 100,000 square meters requested deferment.

But by end-June, the net collection of rentals was back to 97.6%, as both Texas and Georgia re-opened their economies, and collections for the month of July already are close to normal. The nett result of the pandemic on our projected revenue will be negligible and we expect to have fully recovered before year end.

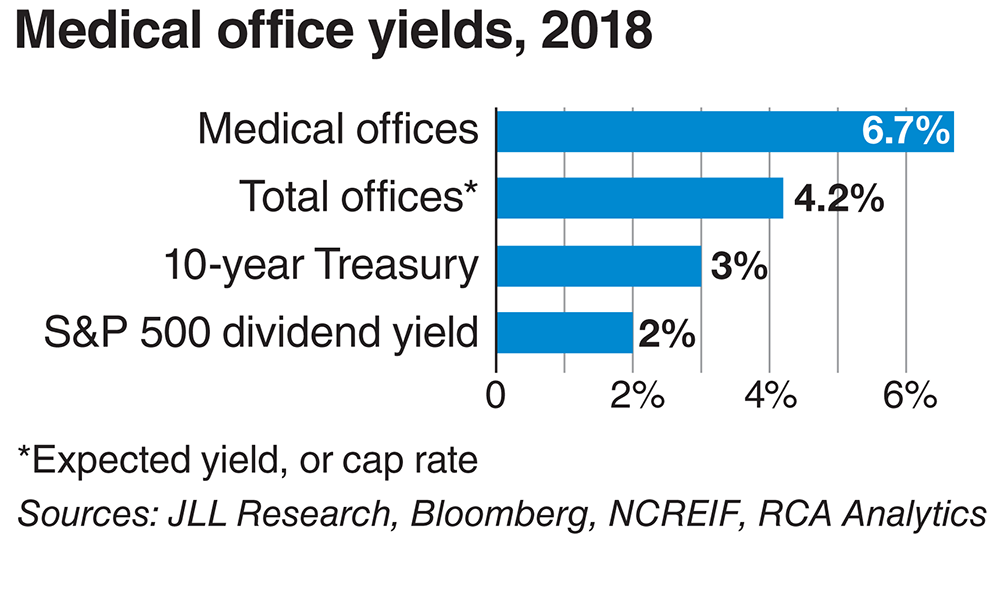

Medical property investment was not an unexpected beneficiary of the Covid-19 crisis. The argument for buying into a building tenanted by medical professionals, especially in the US, makes fundamental sense in the long term. In the US, the aging population is growing and requiring more medical care. An investment delivering a proven 8% p.a. in US dollar dividends paid quarterly, plus a capital gain share at the end of the investment period, is an essential part of a diversified portfolio for South African investors.

Source: Daily Maverick